Introduction

Navigating the dynamic world of cryptocurrency trading can be a daunting task, especially when it comes to understanding the tax implications. Among these, ‘Cryptocurrency Wash Sales’ stand as a crucial concept every crypto investor should be aware of.

Whether you’re in Australia, where I’m based, or elsewhere, beware: tax authorities like the Australian Taxation Office (or ATO for short) are intensifying their crackdown on cryptocurrency wash sales.

No matter where you are, governments worldwide are following suit – a compelling reason to understand and navigate this complex landscape.

Understanding Cryptocurrency Wash Sales

So what exactly is a wash sale?

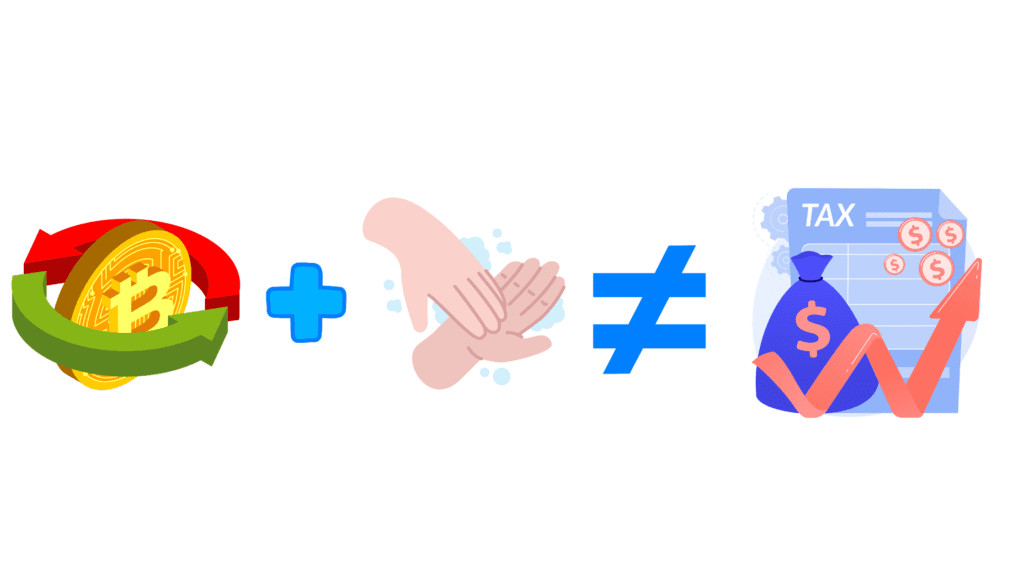

Well, In the financial world, a wash sale occurs when an investor sells a security at a loss and then repurchases the same or a ‘substantially identical’ security within 30 days before or after the sale. While some regulatory bodies may not have provided clear guidance (just yet) on whether the wash sale rule applies to cryptocurrencies, it’s prudent for investors to err on the side of caution.

The Implications of Cryptocurrency Wash Sales

The repercussions of wash sales are far from trivial. If an investor is caught in a wash sale, the loss can’t be claimed on their tax return. Instead, the loss is added to the cost basis of the replacement purchase. This adjustment can lead to higher taxable gains when the replacement cryptocurrency is eventually sold, impacting the overall profitability of the investor’s portfolio.

Identifying a Cryptocurrency Wash Sale

The key to identifying a wash sale lies in meticulous tracking of transactions. A wash sale in the cryptocurrency realm could potentially occur if an investor sells a cryptocurrency at a loss and buys the same or a similar cryptocurrency within a 30-day window. Recognizing such transactions requires a keen eye for detail and a comprehensive understanding of the criteria that the regulatory body (like the IRS) may use to classify a transaction as a wash sale.

Avoiding Cryptocurrency Wash Sales

Avoiding a wash sale can be as simple as waiting at least 31 days before repurchasing the same or a similar cryptocurrency after a sale at a loss.

However, in the fast-paced world of cryptocurrency trading, such a wait may not always be feasible. In such cases, investors can turn to other strategies, such as diversifying their portfolio or hedging their investments, to minimize the risk of a wash sale.

Frequency Asked Questions (FAQS)

Let’s address some of the most frequently asked questions on this topic. Our FAQ section below is designed to provide quick, concise answers to common queries that many of you might have searched for on Google. From understanding the basics of a wash sale to its potential tax implications, we’ve got you covered. So, if you’re looking for immediate answers, this section might just have what you need.

What is a cryptocurrency wash sale?

Does the wash sale rule carry over into the next year?

Can you still do wash sales with crypto?

How can I tell which one of my assets is currently trading at a loss?

Will the wash sale rule for crypto change in the future?

Can you sell crypto for a loss and buy back?

What are the tax implications of a wash sale?

What records do I need to keep to track potential wash sales?

What happens if I fail to report a wash sale?

Conclusion

Understanding and avoiding cryptocurrency wash sales is a vital aspect of successful cryptocurrency trading. While regulatory bodies in your specific country may not have provided clear guidance on the application of the wash sale rule to cryptocurrencies, investors should always err on the side of caution. By staying informed and keeping a close eye on your transactions, you can navigate the complex landscape of cryptocurrency taxation and protect their investments.

But remember, the absolute best course of action you could take to ensure you are abiding by all taxation laws in your region – is to talk to a professional tax accountant who can provide advice that considers your specific circumstances.

Once you’ve navigated the complexities of cryptocurrency wash sales, you might find this guide on how to manage your cryptocurrency taxes in Australia particularly useful. It’s a comprehensive resource designed to help you manage your crypto taxes effectively and stay compliant with the ATO if you’re in Australia. But in saying that, the tool I discuss in this post is applicable to many countries, not just Australia.

If you want to avoid the tedious task of manually reporting your every cryptocurrency transaction, then this would be the post for you!